This weekly market recap is brought to you by Koyfin, a powerful analytical tool that I am proud to partner with. Their platform is entirely customizable for whatever data you want to look at including stocks, ETFs, mutual funds, currencies, economic data releases (one of my personal favorites used often for these posts), crypto, and even transcripts of company events! Click the link above to get a special offer only for Dividend Dollar readers or go give my product review a read if you’re interested!

Weekly Review

The 2023 rally hit a speedbump week as investors may have been looking to take some money off the table after the gains from the last two weeks. Growth and rate hike concerns, which had been put on the backburner to start the year, seemed to be back in play.

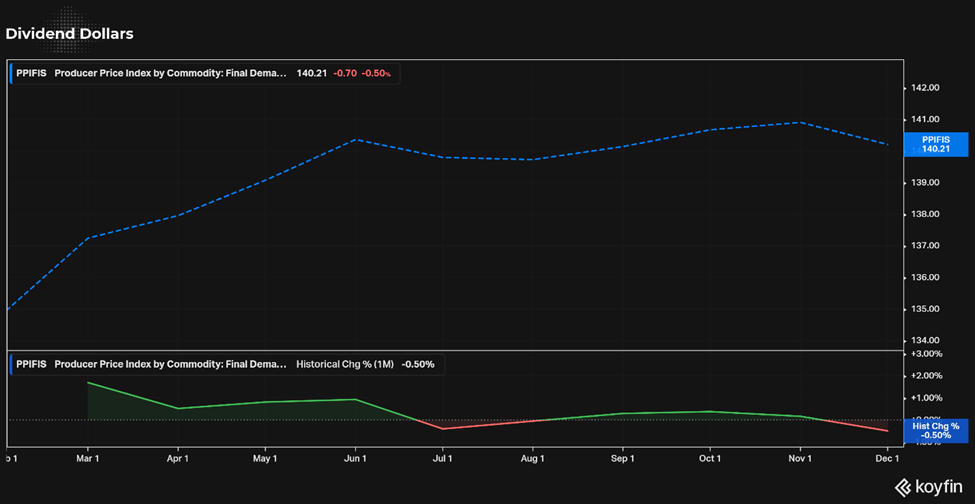

Early on Wednesday, the market initially reacted positively to the slowdown in inflation reflected in the December Producer Price Index (PPI) of -0.5% that beat expectations by 0.4%. Any optimism that may have come from the pleasing PPI report quickly faded as weak retail sales and manufacturing data was released thereafter.

Retail sales fell 1.1% month-over-month in December compared to expectations of -0.8%. This comes off of a revised 1.0% fall in November.

Industrial production fell 0.7% month-over-month in December compared to a -0.1% expectation. This, also, comes off a revised decrease to 0.6% for November.

Following these releases, the main indices sold off on Wednesday. Selling efforts had the S&P 500 take out support at its 200-day moving average. It could be argued that data is suggesting that the Fed is likely to remain on its rate hike path in spite of a weakening economic backdrop, increasing the risk for a policy mistake to trigger a deeper setback and therefor increasing the selling efforts.

Market participants also received official commentary on the economy when the FOMC released its latest Beige Book on Wednesday afternoon. “On balance, contacts generally expected little growth in the months ahead.”

St. Louis Fed President Bullard (non-FOMC voter) added fueled the market’s concerns saying that he would prefer that the Fed stay on a more aggressive path but added that the prospects for a soft landing have improved.

Thursday’s trade, a mostly choppy and sideways day, looked a lot like Wednesday’s trade with investors reacting to more data and commentary pointing towards weakening growth and the possibility of the Fed making a policy mistake.

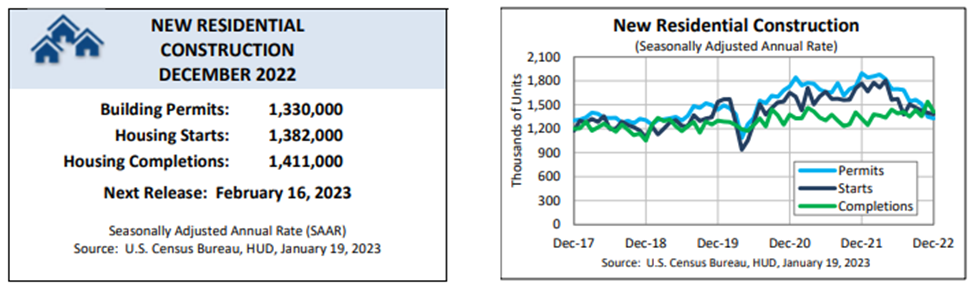

Building permits decreased for the third consecutive month in December to 1.330 million. One surprising positive note out of the report was that single-family starts grew 11.3% month-over-month.

Weekly initial claims were released at the same time, which decreased to 190,000, their lowest level since late September. There are no major weaknesses in the labor market that could put a stop to the Fed’s hiking path.

JPMorgan Chase CEO Jamie Dimon said in an interview Thursday morning “I think there’s a lot of underlying inflation, which won’t go away so quick,” adding that he thinks rates will top 5.0%.

As earnings season progresses, the main concern for the market is the potential that weaker growth will translate to cuts in earnings estimates and downward guidance.

Goldman Sachs ($GS) sold off sharply on Tuesday after reporting below-consensus earnings (Actual EPS 3.32 vs 5.77 Average Estimate) and revenue (Actual 10.59B vs 10.91 Average Estimate), along with increased provisions for credit losses.

So far, however, quarterly results have generally received positive reactions from investors. In contrast to Goldman Sachs, Morgan Stanley ($MS) received a positive reaction despite a Q4 earnings miss.

Another notable earnings report was Netflix ($NFLX), which surged 8.5% on Friday and led to interest in the tech/growth space. It felt like this pushed a sentiment shift and produced the rally effort on Friday.

The rebound effort to close out the week had the Nasdaq Composite recoup all of its losses while the S&P 500 and Dow Jones Industrial Average put a nice dent in their weekly losses. The S&P 500 was able to climb back above its 200-day moving average by Friday’s close.

Only three S&P 500 sectors were green this week — communication services (+3.0%), energy (+0.7%), and information technology (+0.7%) — while the industrials (-3.4%), utilities (-2.9%), and consumer staples (-2.9%) sectors had the largest losses.

The 2-yr Treasury note yield fell two basis points this week to 4.20% and the 10-yr note yield fell three basis points to 3.48%. The U.S. Dollar Index fell 0.2% to 101.99.

WTI crude oil futures rose 2.3% to $81.69/bbl and natural gas futures fell 5.3% to $3.03/mmbtu.

Separately, Treasury Secretary Yellen notified Congress via a letter that the debt ceiling has been reached, prompting the Treasury Department to begin employing extraordinary measures.

Dividend Dollars’ Outlook & Opinion

That’s it for the recap. Now for my opinion!

As I mentioned in the last market update, I predicted a red week this week but that we wouldn’t break below the 100 day SMA. I was correct, but I was not expecting a rally as strong as we got on Friday. After rejecting against the downtrend line and falling under it, we only stayed there for a day before trying again. Truly some wild price action!

My main reason for predicting this is due to my assumption that quarterly earnings this season will show slowing growth. Earnings so far has been mixed, but that slowing growth is starting to as we get deeping into this earnings season. This week 26 companies in the S&P 500 reporting earnings, 15 of them beat consensus EPS expectations. 55 companies of the 500 have reported Q4 results so far and have beaten EPS 69% of the time and revenue estimated 55% of the time.

Year over year, Q4 earnings are -4.5% lower versus a -4.1% estimated from Schwab Managing Director of Trading and Derivatives. Revenues are +7.4% higher year over year versus a 3.8% estimate.

Though there was lots to talk about, this week was a moderate week for economic data materially. The key was the inflation report in PPI which eased quite a bit, it pushed the market higher very briefly before falling down sharply. A slowdown in inflation should be great news for markets since it means the Fed’s rate hikes are having effects. So that brief downturn (and the sideways movement following the CPI) doesn’t make much sense to me, unless you believe inflation expectations were already baked in.

So I believe the movement was mainly a technical one as we rejected hard off the strong downtrend line. After pushing higher through the 50 day SMA last week (dark blue line), the market stalled at the convergence of the 200 day SMA (white line) and the downtrend. The market has failed to break above that line 5 times now.

Given how firmly that line has held, I believe a significant breakthrough above it will be needed before the beginning of the next longer-term uptrend. And next week could be the deciding week for that! Next week is the biggest week for earnings in this earnings season so far.

SPX open interest change for the past week was larger to the put site (call OI +3.0% and put OI +4.4%) as was the aggregate changes in exchange traded products (includes SPY, QQQ, DIA, etc.). This could be interpreted to be bearish. However, open interest participation as a whole is +19.2% greater than 2022 levels which may be bullish for the long term. VIX levels seem neutral in the near-term, however, the VIX IV Gap is lower is moderately bullish.

Price action through Wednesday should be mostly indicative of only earnings releases as there are no noteworthy economic reports through then and the indicators mentioned above are a bit mixed. Thursday brings us the first estimate of GDP for Q4 and durable goods orders for December, both of which can cause a market reaction. Then Friday does a one up and brings us the Core PCE reading for December and a sentiment report for January.

This PCE report is about the only item left that could affect the outcome of the next Fed rate hike, which I predict to be 0.25%, but those results would have to be extremely significant to even put a 0.50% rate hike on the table.

I’m thinking risk off continues into next week after a possible brief approach up to the downtrend line again followed by a rejection down. However, be ready flip sides if earnings beats are common next week as that may be push strong enough to break above. And if we break above its off to the races.

That’s it for my recap! If you would like to see how I am building my dividend portfolio using my predictions/strategy written here, you can read about my buys in my weekly portfolio update on this link.

And if you like updates like this, follow my Twitter or my CommonStock page where I post updates on the economic data throughout the week.

Regards,

Dividend Dollars

One reply on “Stock Market Recap & Outlook (1/20/22) – PPI and Earnings Brings a Whipped Week”

[…] mentioned in the last market update, I was expecting a red week this week and people took money off the table leading into an earnings […]