This weekly market recap is brought to you by Koyfin, a powerful analytical tool that I am proud to partner with. Their platform is entirely customizable for whatever data you want to look at including stocks, ETFs, mutual funds, currencies, economic data releases (one of my personal favorites used often for these posts), crypto, and even transcripts of company events! Click the link above to get a special offer only for Dividend Dollar readers or go give my product review a read if you’re interested!

Dividend Dollars’ Outlook & Opinion

Last week we ended the outlook with neutral outlook call, which appeared to be correct up until mid-week. Q1 earnings season is nearing a close after this week, with 94% of companies having reported. 78% of companies reported a positive EPS surprise and 76% reporting positive revenue surprises. Despite the positive surprises, blended earnings results look to be -2% lower than the prior quarter, marking a second straight decline in earnings for the S&P 500.

What’s even more interesting is that more S&P 500 companies than normal have commented on a “recession” during their earnings calls. 107 companies used the term, which beats the 5 year average of 77 and 10 year average of 59 by a considerable margin. Unsurprisingly, the financials sector discussed it the most. However, it should be noted that this statistic appears to have peaked in Q2 of 2022.

Regardless of the earnings fun fact, this was a slow week for market data (yay these weeks make my job easier)! Initial jobless claims came in lower than expected and lower than last week, showing that jobs are still hot. The reading came in at 242k, the 15th consecutive week it has been above 200k. Housing data continues to come in hot. Retail, on the other hand, fell flat of expectations but was still positive. Next week we have new home sales on Tuesday, jobs, GDP, and pending home sales on Thursday, and PCE and sentiment on Friday.

For technicals, stocks continue to shock and confuse bears and naysayers. They continue to perform better than expected, especially with the unresolved debt ceiling battle. With a 1.8% gain on SPX this week, the chart has reached its strongest position year-to-date. It closed well above all major averages and is poised to break above the 4,200-resistance level (a level that has held for 7 straight weeks). At this point, falling back to the bear market region would require a 15% drop, while a rally to the bull region is now only 2% away.

Most indicators had positive moves this week, including the SPX open interest change, the VIX implied volatility gap, and the VIX futures levels. The composite levels of the indicators are primarily neutral or moderately bullish.

As for next week, the most important item is the PCE reading, as it is the Fed’s inflation gauge and a number of Fed speak this week reaffirmed the fact that their decision would be led by data. If we want a rate pause, this reading had better be good. However, since the next Fed meeting is still three weeks away, the PCE may not matter much in the near-term. If we assume this weeks positive moves were based on debt-ceiling optimism, it may not be shocking to see a quick decline if/when it happens. That may seem contrarian, but it is a buy-the-rumor and sell-the-news approach.

If there is no debt ceiling resolution, the whole picture points to more bullishness. If/when the debt ceiling is breached or lifted, volatility is the expectation, but direction will be determined by the catalyst.

Weekly Market Review

Summary:

The major indices gained this week, breaking a 6-week period of less than 1% moves for the S&P 500. The index reached new closing and intraday highs for the year but failed to maintain a position above 4,200, a level of strong resistance. While mega-cap stocks supported the index’s performance, the breadth of gains was wider this week. The S&P 500 rose 1.7%, while the Vanguard Mega Cap Growth ETF ($MGK) up 2.9% (why did I sell!) and the Invesco S&P 500 Equal Weight ETF (RSP) up 1.0%.

Signals were mixed this week. Optimism about a debt ceiling deal emerged after President Biden’s meeting with congressional leaders, but it waned when debt limit talks were paused according to Jake Sherman, a reporter for Punchbowl News. Some Federal Reserve officials expressed hawkish views, with Dallas Fed President Logan stating that current data doesn’t support a pause in June and St. Louis Fed President Bullard acknowledging the need for further rate hikes due to persistent inflation.

Treasury yields saw a decrease in the safety premium, especially at the short end of the curve, as investors considered the possibility of the Fed raising rates at the June FOMC meeting. The 2-year note yield rose by 29 points to 4.27%, and the 10-year note yield increased by 23 points to 3.69%. The bond market also reacted to positive sentiment about debt ceiling talks and favorable performance in regional bank stocks, with the SPDR S&P Regional Banking ETF (KRE) rising 7.8% and Western Alliance (WAL) experiencing a 24.9% increase on news of deposit growth.

Earnings reports from key retailers marked the week, with mixed reactions seen for Dow components Home Depot ($HD) and Walmart ($WMT). Target ($TGT) received a positive response, while Foot Locker ($FL) faced a significant decline of 27% after reporting disappointing earnings and issuing dismal guidance. The majority of S&P 500 sectors recorded gains, with information technology, consumer discretionary, communication services, and financials leading the way. However, the utilities sector experienced the largest decline, followed by real estate.

Monday:

Monday ended on a relatively positive note, although the price action was dismal with below-average volume. The major indices closed near their daily highs, posting modest gains. While there was initial weakness in mega-caps, some stocks in this category rebounded to finish with gains, contributing to the overall performance. Meta Platforms ($META) stood out with consistent outperformance after receiving an upgrade, while the Vanguard Mega Cap Growth ETF ($MGK) closed with a 0.2% gain.

The market’s inclination to buy mega-cap stocks reflected concerns about the uncertain debt ceiling situation, as President Biden’s meeting with congressional leaders on the topic approached. Regional bank stocks experienced a rally, providing support to the broader market. The SPDR S&P Regional Banking ETF ($KRE) had a 3.2% gain, and the S&P 500 financials sector closed near the top of the leaderboard with a 0.8% increase.

In terms of M&A activity, Newmont plans to acquire Newcrest for approximately $19 billion, and Oneok plans to acquire Magellan Midstream Partners for around $18.8 billion, including assumed debt. The market also saw positive regulatory developments, as EU regulators approved Microsoft’s acquisition of Activision. On the economic data front, the New York Fed Empire State Manufacturing Survey had a significant decline, with the new orders index dropping 53 points to -28.0, pointing to a sharp decrease in demand.

Tuesday:

The market looked in step with previous days, with limiting factors keeping it in check while gains from mega-cap stocks provided some support. However, the major indices closed near their lowest levels of the day following news that President Biden would be cutting his G-7 trip short. There was no information available about Tuesday’s debt ceiling meeting, but House Speaker McCarthy noted that the two sides remained far apart, while Senate Majority Leader Schumer emphasized the need for bipartisan agreement to avoid a default.

Despite losses in the overall market, gains in the mega-cap space helped mitigate the decline. The Invesco S&P 500 Equal Weight ETF ($RSP) dropped 1.4%, while the Vanguard Mega Cap Growth ETF ($MGK) recorded a 0.1% gain. The Dow Jones Industrial Average experienced the largest decline, partly due to Home Depot’s disappointing fiscal Q1 sales and guidance.

Retail sales data for April were released, indicating a 0.4% increase in total retail sales, but adjusting for inflation showed essentially flat sales, implying weaker demand. China also reported weaker-than-expected retail sales, industrial production, and fixed asset investment for April, contributing to concerns about global growth. Additionally, the FTC’s lawsuit to block Amgen’s acquisition of Horizon Therapeutics weighed on the stock and added further headwinds for equities.

Economic data for Tuesday included the April retail sales, industrial production, and the NAHB housing market index.

Retail sales came in at +0.4%, under the expected 0.7%. These readings are not inflation adjusted, so when making that adjustment, the reading is closer to flat. Growth in sales, therefore, was mostly due to price increases and not necessarily an increase in demand.

The industrial production report came in at +0.5%, compared to a flat expectation. Capacity came in just 10 basis points under the expectation at 79.7%. Manufacturing output bounced back in this reading, supported by gains in the output of vehicles and parts, defying a hard-landing economic scenario.

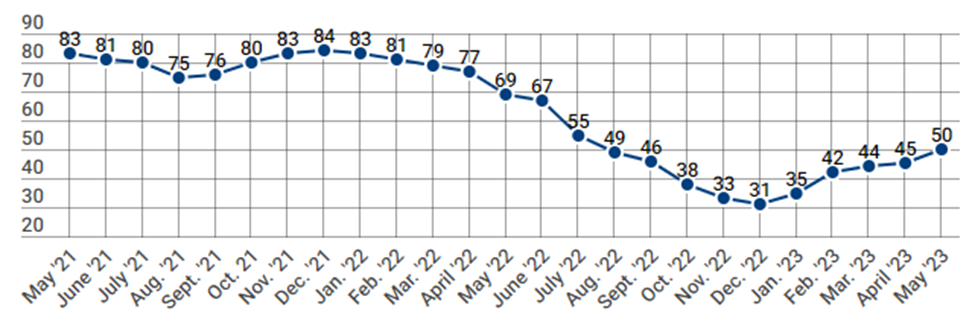

The NAHB housing index came in at 50, the 5th straight monthly increase and the highest level since July 2022. The index was expected to be flat at 45. Current sales, expectations, and buyer traffic were all higher.

Wednesday:

The stock market was soft right out of the gate, but found upside momentum. Gains built, aided by some short-covering activity. The major indices all closed near their best levels of the day.

Positive responses to earnings and other corporate news, along with an emerging hope that the president and congressional leaders are more aligned with debt ceiling negotiations, pushed things higher. Still, no deal has been reached and uncertainty remains in play. That uncertainty was not enough to offset Wednesday’s strong showing, a potential pro-cyclical bias.

Many stocks came along for the rally; 9 of the 11 S&P 500 sectors closed green. The financials sector lead with 2.1%. This came after Western Alliance ($WAL) said its deposits have increased by more than $2 billion since the end of the first quarter. This news put a bid in the bank stocks and the SPDR S&P Regional Bank ETF (KRE) jumped 7.4%.

Economic data included the MBA mortgage applications, housing starts and building permits.

The Mortgage Applications Index fell 5.7% with purchase applications falling 4.8% and refinancing applications falling 8.0%.

Total housing starts increased 2.2% MoM in April to a seasonally adjusted annual rate of 1.401 million compared to a consensus of 1.405 million. Single-family starts were up 1.6% MoM, but only because of a strong 59.5% increase in the West; single-family starts fell in all other regions.

Building permits fell 1.5% MoM to 1.416 million from an upwardly revised 1.437 million in March. Single-unit permits rose 3.1% MoM, led by gains in all regions. The weakness in permits was driven by a 9.7% decline in permits for 5 units or more.

The key takeaway here is that single-family starts and permits were up, which is a positive given the tight supply of existing homes for sale. Even so, the constraints of high financing rates and high prices are evident in single-unit starts being down 28.1% year-over-year and single-family permits being down 21.2% YoY.

Thursday:

It was another good day for stocks, building on Wednesday’s gains. The major indices traded in mixed fashion until a late afternoon surge higher. That move saw the S&P 500 break the 4,200 level for the 1st time since August 2022. Ultimately, the S&P 500 closed at its best level of the year, just a whisker shy of 4,200.

The midday lull was probably ongoing hesitancy about the debt ceiling. House Speaker McCarthy said he “sees a path” to getting the debt limit bill on the House floor for a vote next week, yet other press reports suggest a debt ceiling deal won’t be easy to reach.

Market participants were also reacting to some mixed economic data, including lower-than-expected jobless claims, a better-than-expected Philadelphia Fed Index for May, and weaker-than-expected existing home sales and leading economic indicators for April.

Nonetheless, the afternoon rally was fairly broad based, ratcheting up as the mega cap stocks took another leg higher along with the semiconductor stocks both having several names reaching new 52-week highs.

Friday:

The stock market kicked off this options expiration day on an upbeat note, but ultimately rolled. Opening gains had the S&P 500 back above the 4,200 level before the market turned lower middaywhen Fed Chair Powell began speaking at a panel discussion regarding perspectives on monetary policy.

However, stocks seemed to be responding to worries about the debt ceiling and regional banks, rather than Mr. Powell’s comments. Briefly, Mr. Powell said that inflation is “far above” the Fed’s objective, but also said that rates may not have to rise as much because of credit conditions. These views were comparable to what he shared during his press conference following the FOMC meeting earlier this month, so they weren’t necessarily surprising.

What was surprising was the prior mentioned tweet from reporter Jake Sherman that “debt limit talks between the White House and House Republicans have been paused, per multiple sources involved in the talks.”

Ultimately, the major indices were able to climb somewhat off their lows to close with modest losses; however, the S&P 500 remained pinned below 4,200 on a closing basis.

That’s it for my recap! If you would like to see how I am building my dividend portfolio using my predictions/strategy written here, you can read about my buys in my weekly portfolio update on this link.

And if you like updates like this, follow my Twitter or my CommonStock page where I post updates on the economic data throughout the week.

Regards,

Dividend Dollars