This weekly market recap is brought to you by Koyfin, a powerful analytical tool that I am proud to partner with. Their platform is entirely customizable for whatever data you want to look at including stocks, ETFs, mutual funds, currencies, economic data releases (one of my personal favorites used often for these posts), crypto, and even transcripts of company events! Click the link above to get a special offer only for Dividend Dollar readers or go give my product review a read if you’re interested!

Weekly Review

The market seemed to be in a turkey coma as there wasn’t much action in the first half of the week. The market was choppy while waiting for Fed Chair Powell’s speech on Wednesday and the key economic data to follow.

The market liked what it heard in Mr. Powell’s speech and things took off in a big way on Wednesday off of his hints that the Fed may slow the pace of rate hikes.

Some will argue that he actually loosened the screws a bit. I would argue he didn’t even bring his toolbox. The market, which was waiting for a to be hit like a nail by a hammer, was relieved when he did not.

This became a rally catalyst that caused some short-covering and some chasing action as the S&P 500 broke above key resistance at its 200-day moving average.

Powell’s actual speech repeated just about everything he said following the November FOMC meeting. Some added attention was paid to his summation that “the ultimate level of interest rates will be somewhat higher than previously expected” versus the original contention that “the ultimate level of interest rates will be higher than previously expected.”

Mr. Powell’s talk (and tone) presumably weakened the fear of another 75-basis point rate hike. Granted the fed funds rate is still going higher from current levels, but market participants can smell a peak in the policy rate around 5.00% in the first half of next year. If the FOMC elects to raise the target range by 50 basis points at the December meeting, the target range will be 4.25-4.50%.

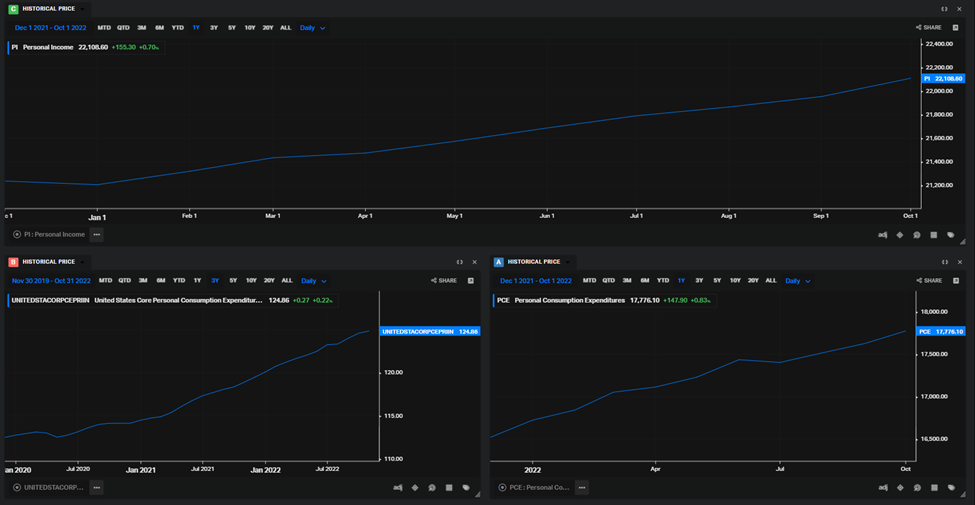

On Thursday, market participants received the October Personal Income and Spending Report, which favored the “smaller” rate hike at the same time it favored a soft landing possibility.

Personal income increased 0.7% month-over-month in October and personal spending jumped 0.8%. The PCE Price Index was up 0.3% month-over-month and the core-PCE Price Index, which excludes food and energy, increased 0.2%.

On a year-over-year basis, the PCE Price Index was up 6.0%, versus 6.3% in September, and the core-PCE Price Index was up 5.0%, versus 5.2% in September.

The big rally effort slowed as market participants contended with the notion that the upside moves might have been an overreaction and that the growth environment is going to be challenging given the past rate hikes and the rate hikes that are yet to come.

A 49.0% reading for the November ISM Manufacturing Index, which is the first sub-50% reading (the dividing line between expansion and contraction) since May 2020, hurt some of the rebound enthusiasm.

The November employment report on Friday also tested the rally. Nonfarm payroll growth was higher than expected, the unemployment rate held near a 50-year low of 3.7%, and average hourly earnings increased at a robust 0.6% month-over-month, leaving them up 5.1% year-over-year.

The report itself was good news from an economic standpoint, yet the market saw it as bad news as it gives more room for the Fed to slow the economy with rate hikes. The report signals higher for longer with respect to the target range for the fed funds rate.

The initial retreat following the employment report saw the S&P 500 breach its 200-day moving average, but by Friday’s close the index reclaimed a position above that level. All in all, this week was a win for the bulls given that the market showed nice resilience to selling efforts and the S&P 500 held the line at that key technical level, next is the downward trend line 👀

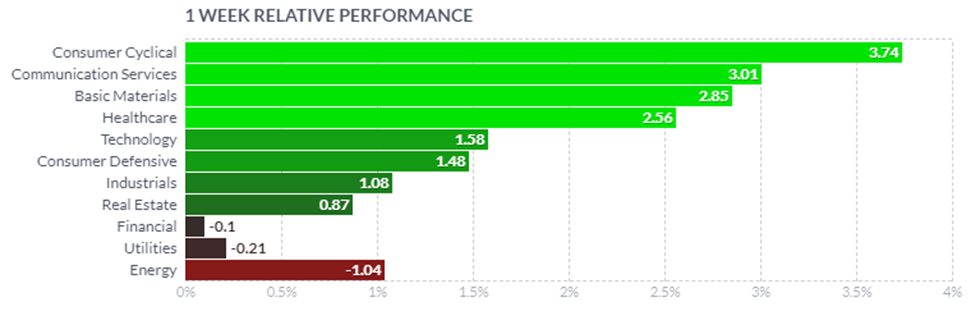

8 of the 11 S&P 500 sectors closed with a gain on the week. Communication services and consumer discretionary enjoyed the biggest gains. Energy, utilities, and financials were the lone sectors in the red by the end of the week.

In the Treasury market, there were big down swings predicated on the thinking that maybe the Fed won’t have to raise rates as high as feared. The continued inversion along the yield curve reflects the festering concerns about the Fed raising rates into a weakening economy and inviting a recession. The 2-yr note yield fell 19 basis points to 4.29% and the 10-yr note yield fell 18 basis points to 3.51%.

Dividend Dollars’ Opinion

That’s it for the recap. Now for my opinion!

As I stated last week, we just barely broke above the 200-day EMA. We opened this week below it and would have finished there if the market hadn’t rallied so hard off of Powell’s speech. I even called that we could gap fill to the 4,080 area, and we did!

I’m not trying to make a habit out of predicting things, just simply share with you what I’m noticing. And I’m noticing that an end of year rally could push us slightly higher to the mother of all trendline’s. The red line in my chart below has been rejected every time since ATHs.

We could very easily stay fighting for that trend line through the end of the year before a significant breakout happens. But when it does happen, the direction is anybody’s guess. My money is on down.

Here’s why: what did Powell say on Wednesday that warranted a 3% surge on the S&P? Signals of slowing rate hikes are nice… but the probability of a 50-point rate hike in December has not changed. The CME Fedwatch tool showed a 75% probability of a 50-point hike last week. The probabilities for a smaller hike in the February meeting were fairly unchanged as well.

People all over are anticipating a “Fed Pivot”. But the Fed is far from pivoting. A Fed Pivot happens when the Fed reverses their monetary policy stance and occurs when the underlying economy has changed to such a degree that the Fed can no longer maintain its policy.

What on Wednesday suggested that this was the case? We are still a ways away from the peak rate and even then we will be at that rate for sometime before a rate cut is imminent. So why did the market bounce as it did following the speech?

The main reason is that expectations were low. We expected him to stay hawkish, instead we got optimistic. To me, playing the expectations game is silly. Rates are rising, and they will be staying there for a while. This will eat at companies’ earnings and sooner or later will be reflected in stock prices.

Be ready for deals, the technical indicators say a dip is coming. Worse yet, a recession is still not out of the picture.

I think that inflation is still a larger problem than the market anticipates. We have seen the market move higher on “better-than-expected” inflation readings where inflation is still over 7% and CPI has yet to peak.

The Fed may lessen the size of the rate hikes, but we are a long way away from ever having rates decreased. Till then, the market is at risk of entering a very serious recession.

The Fed is trying to engineer a soft-landing and so far they have done a great job of it.

However, the longer rates stay high, the closer we may get to seeing the Fed’s planned economic slow down go too far. GDP, employment, real incomes, etc. These things will start to waiver, earnings will start to miss, and the market will start to look quite overbought at these levels which will kick off some serious selling and capitulation.

Because of this, I am short with a position in $SDS and $SPXS and am holding more cash than normal. The short is only 2% of my portfolio and the cash is 10%. I’ll be adding to this short and cash position through to the end of the year if we remain trending up, but I think we are getting closer to a flip

I constantly make moves in my portfolio according to this thesis. You can read about these moves in my weekly portfolio update here.

And if you like updates like this, follow my Twitter or my CommonStock page where I post updates on the economic data throughout the week.

Regards,

Dividend Dollars