This weekly market recap is brought to you by Koyfin, a powerful analytical tool that I am proud to partner with. Their platform is entirely customizable for whatever data you want to look at including stocks, ETFs, mutual funds, currencies, economic data releases (one of my personal favorites used often for these posts), crypto, and even transcripts of company events! Click the link above to get a special offer only for Dividend Dollar readers or go give my product review a read if you’re interested!

Weekly Market Review

The January rally carried on as investors received more market-moving earnings results and data releases this week. The positive bias had the S&P 500 get back above its 200-day moving average and stay there all week.

Things got started on an upbeat note on Monday after an article by Nick Timiraos (chief economics correspondent for WSJ and Fed’s assumed preferred source for divulging information to) highlighted the possibility of the Fed pausing its rate hikes this spring.

Monday also brought us a survey of businesses by the NABE that conveyed a lower possibility (56% vs nearly two-thirds before) of the U.S. being in a recession or entering one.

The market hit a speed bump on Tuesday with a lot of divergent stock prices for a number of NYSE-listed stocks including Morgan Stanley ($MS), AT&T ($T), Verizon ($VZ), Nike ($NKE) and more. The abnormality quickly led to volatility halts brining many of us to wonder what was going on. The official explanation turned out to be an “exchange-related issue.” The issue seemed to be resolved quickly with announcements of some trades will be declared null.

Defense-related companies Lockheed Martin ($LMT) and Raytheon Technologies ($RTX) reported positive quarterly results.

Market strength was offset by some disappointing earnings/guidance from the likes of Verizon ($VZ), 3M ($MMM), Union Pacific ($UNP), and General Electric ($GE), along with the news that the U.S. filed an antitrust lawsuit against Google over alleged dominance in digital advertising.

Price action on Wednesday was integral to keeping the rally alive this week. Valuation concerns from Microsoft’s ($MSFT) disappointing fiscal Q3 outlook and expected growth deceleration for its Azure business fueled a broad retreat to kick off the session.

Investors also had a negative reaction initially to results and/or guidance from the likes of Dow component Boeing ($BA), Texas Instruments ($TXN), Kimberly-Clark ($KMB), and Norfolk Southern ($NSC).

Buyers showed up quickly after the S&P 500 dipped below its 200-day moving average to push the market higher. Most stocks either narrowed their losses or completely recovered and closed the session with a gain.

After the strong reversal on Wednesday, Tesla ($TSLA) reported strong quarterly results and outlook, which helped the rebound in the mega cap space, and Chevron ($CVX) announced a massive $75 billion stock repurchase program announcement.

There was also a number of positive data releases Thursday that helped support a positive bias. The Advance Q4 GDP Report increased at an annual rate of 2.9% in the fourth quarter of 2022. The second estimate will be released towards the end of February.

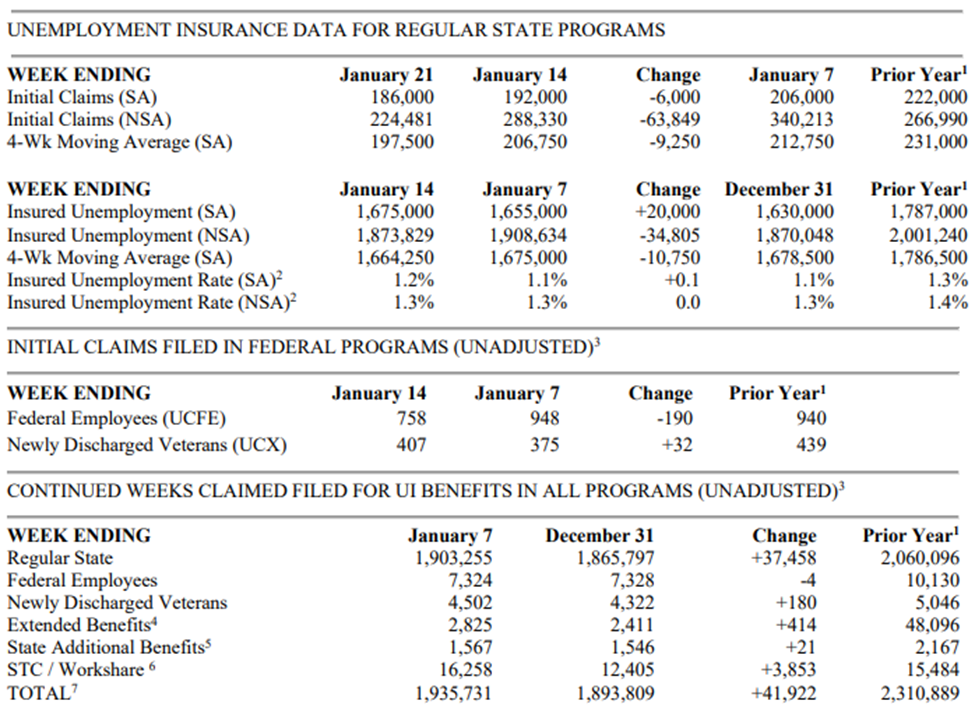

Weekly initial jobless claims unexpectedly decreased by 6,000 compared to the previous week. The current level of 186,000 is well below the 4-week moving average of 197,500.

December durable goods orders came in better than expected, as well. Orders increased 5.6% month over month to $286.9B versus an estimated 2.5%. This is especially a good reading compared to a -1.7% decrease from revised numbers last month. Excluding defense, the durable goods orders were up 6.3% for the month. Inventories, up for 23 consecutive months at this point, increase again by 0.7%.

The rally effort continued on Friday despite Intel ($INTC) reporting ugly results and guidance, KLA Corp. ($KLAC) issuing below-consensus guidance, Chevron ($CVX) missing on earnings estimates, and Hasbro ($HAS) issuing a Q4 profit warning.

On Friday, the PCE Price Index was released. Results were up 0.1% month-over-month while the core-PCE Price Index, which excludes food and energy, was up 0.3%, as expected. That left the year-over-year changes at 5.0% and 4.4%, respectively, versus 5.5% and 4.7% in November.

There was a sharp pullback before Friday’s close, as people took money off of the table heading into a big week of earnings next week from Alphabet ($GOOG), Apple ($AAPL), Amazon ($AMZN), and Meta. Other catalysts include the FOMC decision and the January Employment Report.

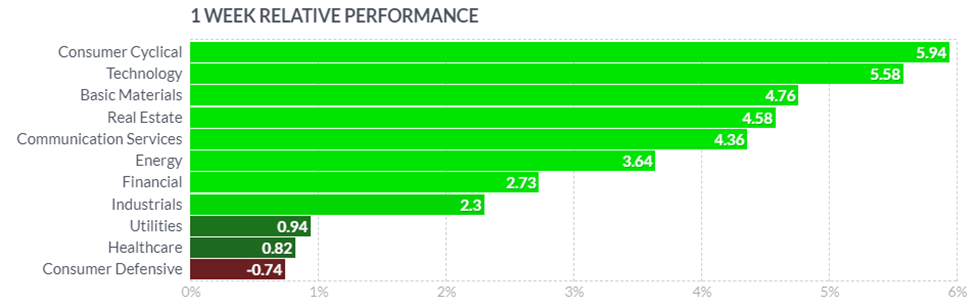

Only two S&P 500 sectors registered losses this week — utilities (-0.5%) and health care (-0.9%) — while the consumer discretionary (+6.4%), information technology (+4.1%), and communication services (+3.3%) sectors led the outperformers.

Dividend Dollars’ Outlook & Opinion

That’s it for the recap. Now for my opinion!

As mentioned in the last market update, I was expecting a red week this week and people took money off the table leading into an earnings heavy week. My other, less anticipated call, was that stocks could break above the downtrend line. This was the outcome to took precedent.

Stocks looked to trend higher this week and was supported by better than feared (notice the “better than feared” vs “better than expected” clarification was intentional) earnings reports and economic data! No data report this week was too good or too bad, and more items like this support the chance of an actual soft landing for the economy. We will have a better feeling for this next week after the FOMC meeting, but in the meantime bias is positive.

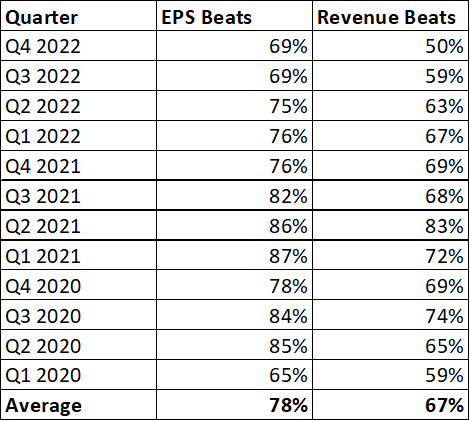

147 of the S&P 500 companies have released earnings so far. 50% have beat on top line expectations and 69% have beat on bottom line. The 50% beat rate, should it hold, would be the lowest top line rate since before the pandemic. Next week is a big earnings week and will give us more information on potential earnings recession. This information is tracked using MarketBeat.

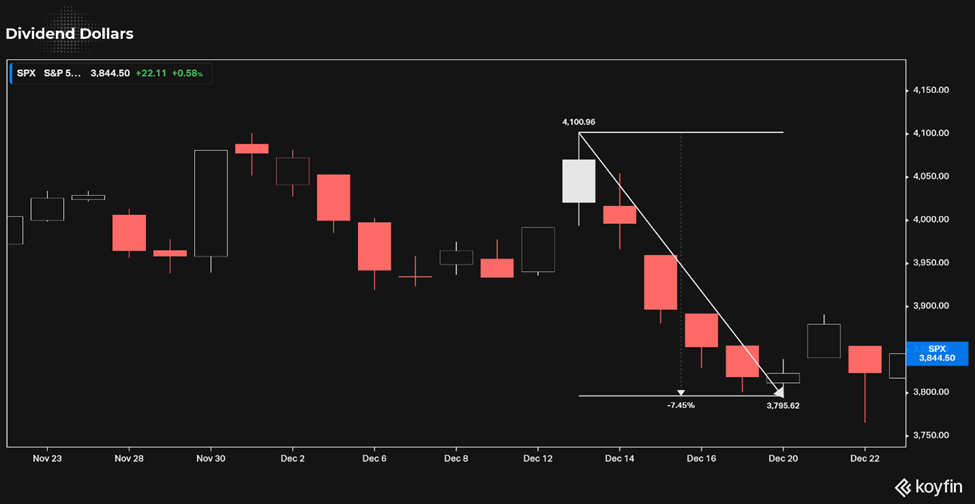

The S&P chart has turned bullish as the market pushed above the downtrend and put some space between price and the SMA 200. We have had the highest number of daily closes above the 200 day SMA in 2023 so far since last spring. The next level I see is around 4,080 that has rejected three times.

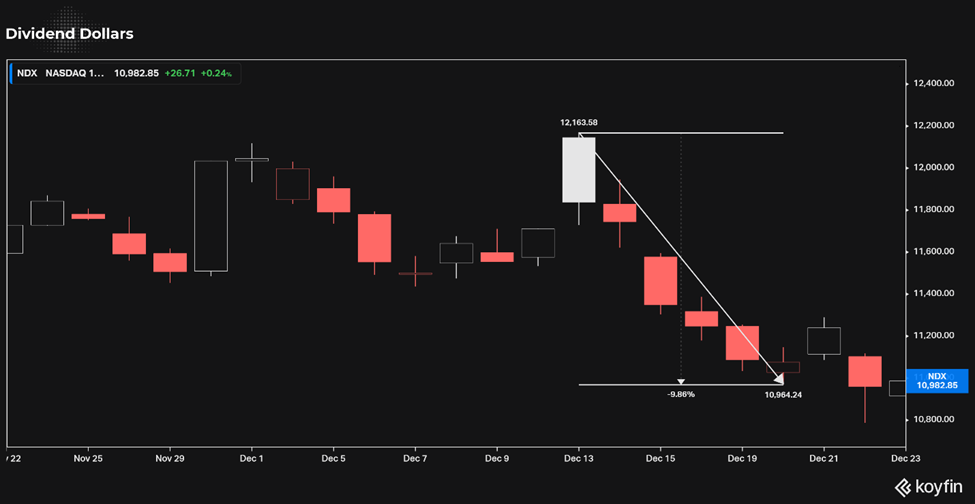

Similarly, the Nasdaq Composite index has a level a 11,617 to get over. It is also approaching the change to break above the 200 day SMA for the first time in a year. Additionally, the index is above is 11,500 resistance level. It looks bullish but the coming earnings from mega-cap tech names have the potential to move it.

Overall, stocks are riding recent bullish momentum and are being supported by technical developments. The market appears to be hopeful that the Fed will show a less aggressive stance on rates. We have seen this optimism in the past before, but we haven’t seen the Fed move into a stock friendly stance. Maybe that happens at the next meeting, maybe we get more information on potential rate hike path.

We will see what happens with the Fed next week and will have a better feel of what’s going on in tech. With VIX as low as it is, a slurry of stocks reaching 52 week highs, decent earnings and data, the bulls appear to be in control for the near term. Potential for volatility next week is high. I think the market is moderately bullish in the first of the week then could be volatile in either direction depending on those factors.

That’s it for my recap! If you would like to see how I am building my dividend portfolio using my predictions/strategy written here, you can read about my buys in my weekly portfolio update on this link.

And if you like updates like this, follow my Twitter or my CommonStock page where I post updates on the economic data throughout the week.

Regards,

Dividend Dollars