This article is brought to you by 3X Trading, a community that highlights experience and expertise of the professionals within. While other groups rely on algorithms or inexperienced traders, 3X relies on its team of seasoned professionals to navigate markets, providing you with analysis, classes, and a personal service to ensure you are always informed and making good trading decisions, for any strategy. Join the Discord server for free and learn from dividend investors and day traders alike. I frequently share analysis and insights throughout the week, so I hope to see you in there! Thank you Discord members @Jenlevit and @Alladin for working on the marketing and the charts of this piece!

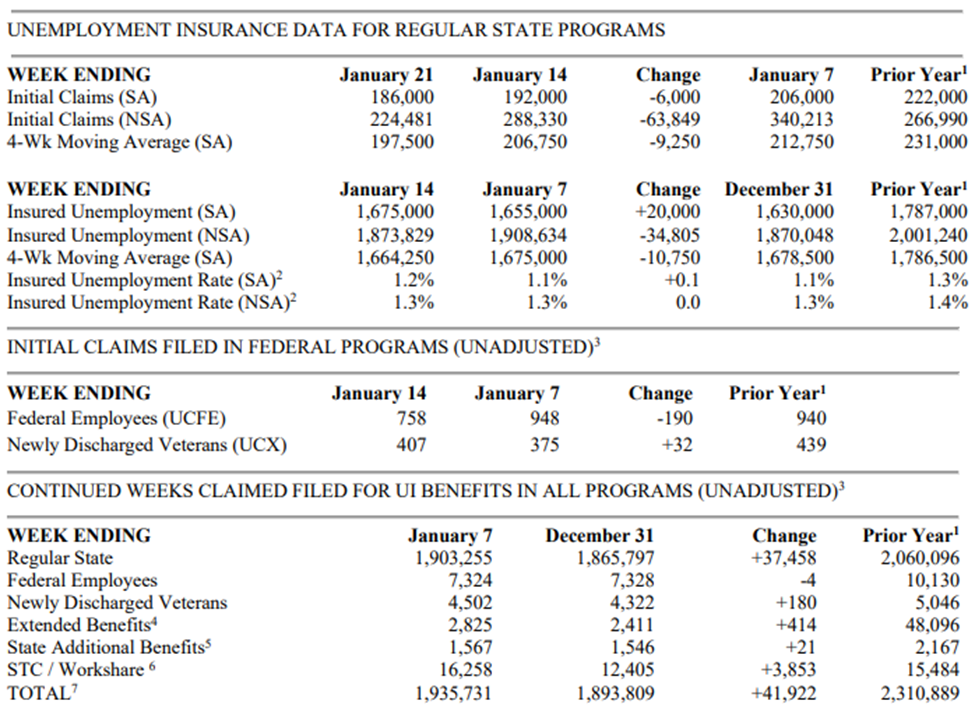

Market Cycle

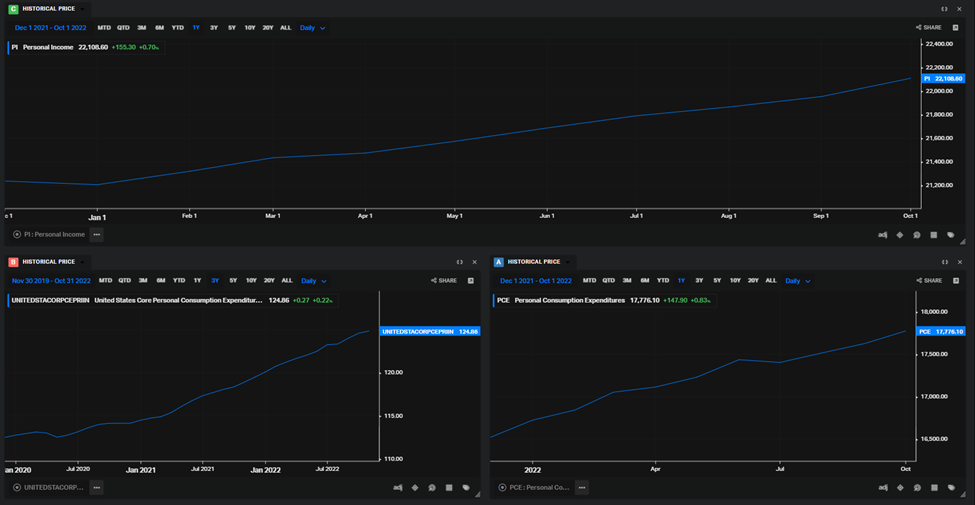

The market is in a weird spot to kick off 2023. So far, this year feels like the inverse of 2022. High inflation, which defined most of the last year, seems to have given way to a narrative of falling inflation. Wages data, small business surveys, CPI, and ISM data (all items we cover regularly on the weekly market recaps) suggest softening.

The graph above is called “The Psychological Pitfalls Of A Market Cycle”. It’s broken up into four distinct areas indicated by the colors. The orange color on the far left is the Mark Up phase of a cycle, next is Distribution, followed by Mark Down, and ending with Accumulation in the dark red before the cycle repeats again with Mark Up.

We have had three consecutive inflation reports that showed no major inflation concerns. In fact, two of those three reports actually contained negative surprises! The Fed on Wednesday acknowledged weakening inflation while also mentioning that they still have work to do. Anyways, it is clear that the market’s narrative has shifted to declining inflation and that the Fed will pivot dovish sooner or later. Therefore, now is a great time to look for some early cycle outperformers.

The Soft Line Industry

Before I dive into why this sector could be good for cycle moves in the near term, lets discuss what soft lines are. If you google what the soft line industry is, you will see a site that says they sell primarily soft merchandise. Not a very helpful explanation, but it is technically correct and is a term that is used in retail quite often.

Soft lines are retailers that sell smaller items that are usually soft. Consumer items like linens, clothing, shoes, bags, towels, mats, pillows, and sometimes even beauty products. These kinds of goods may be called soft items. They are typically more difficult to handle in the supply chain than hard goods. Hard goods are stackable, easy to store, and easy to transport while soft goods need to be packaged carefully, they can wrinkle, they need to be presented aesthetically in stores, and are more sensitive to restocking.

Soft Line – Early Cycle Mover

Now back to the cycle. The uncertain backdrop of the economy appears to be closely tied to the health of the US consumer. With that said, I believe the soft line industry is at an interesting value point. Morgan Stanley’s US Soft Lines Retail Equity Analyst, Alex Straton, called the coming year a ‘tale of two halves’ in a Thoughts on The Market Podcast last week when discussing soft lines.

What they meant by this is that the first half of what retailers are facing is harder expectations from an income statement perspective caused by an ongoing excess inventory overhang (Nike’s large inventory in the end of 2022 is a great example of this) and possible recessionary conditions from a macro perspective. An article from Morgan Stanley claimed that census forecasts for the S&P 500 have earnings growth at almost 4%, this is overly optimistic in their view. Consensus earnings growth expectations specifically for soft lines are even more optimistic at 15%.

These stocks can be moved significantly based on earnings revisions. If we have negative earnings revisions ahead based on the assumption that expectations are unrealistic, it’s likely that the stocks move downwards from here, hitting a bottom sometime in the first half of the year.

The second half of the year presents a very different story – hence the tale of two halves. If earnings revisions/expectations become more realistic, the industry will be in a position to more easily meet top line returns and margins may receive year-over-year relief. This relief may come from falling fright costs, falling price of cotton, promotions, etc. On top of that, as we go through the year, inventory should mostly reach normalization. Lastly, a recovering macro perspective should be more solidified in the second half of the year. With this improving backdrop and the fact that soft lines are early cycle outperformers, they could quickly pivot off the bottom and see gains.

It is impossible to ever call a bottom accurately and consistently on anything. But given the case for the industry turn around as we have laid out, there are a few data points to keep an eye on to help you realize when the time to initiate might be near. The first indication is 2023 guidance, and we should get more information on this in the coming weeks as earnings season continues.

The other item that we will spend more time explaining is inventory levels. Cleaner levels are essential to having a view on how long the margin risk that hit retailers in the second half of 2022 could potentially linger into this year. Last year, there was a lot of market discussion around the inventory problem. It was seen as a key risk to earnings with oversupply and lagging demand creating the perfect storm for pressuring margins.

Today, retailers have made good progress of working down inventory levels in the third quarter of 2022, but there’s still much room to go. Look at the examples below from Tapestry’s ($TPR) Q1 2023 earnings report, Ralph Lauren’s ($RL) Q2 2023 earnings report, Nike’s ($NKE) Q2 2023 earnings report, and VF’s ($VFC) Q2 2023 earnings report. What we would rather see here is that inventory levels are in line with forward sales growth.

How To See The Opportunity

As we look across the soft line space for opportunities to take advantage of for an early cycle move, make sure that you’re sticking to sound fundamental and intangible analysis. What I mean by fundamental is if the company is growing or outperforming (beauty stores like Ulta are a great example of this), look for diversification in selling channels, be aware of company events such as restructuring or leadership changes, understand if their margins reasonable, and look to see if investors are rewarded with buybacks, dividends, and/or sufficient price appreciation. What I mean by intangible is if the company has a strong brand, if the brand has value, if that brand value had an upward trajector, and do the products speak to the consumer.

If you can answer most of these items in a positive light, then you may have located a good company for this early move.

For me, certain subsectors of this industry particularly interest me and others that don’t. One to avoid, in my opinion, is activewear. These items saw strength in Covid as people gained a higher affinity for staying healthy, exercising, and taking care of their bodies. Long term, the category has really nice upside potential, but for the purposes of getting early cycle returns, the lingering strength from Covid may negate the strategy.

My other point is on mid-tier brands vs luxury/high-tier brands. A debate as old as time. I lean high-tier, for a couple of reasons. One is that higher wealth consumers will be less affected by a recession if one happens. The global economy is growing, China is opening, and India looks to be on the verge of its most performative decade ever. These items will boost attention to and desire for world-renown luxury brands. Another point I have is called revenge shopping. The Economist touched on this phenomenon which is where people are more willing to splurge on high-end items currently because they have been pinching pennies and living a stressful life since Covid that they feel they should treat themselves.

My Picks

Having said this, here are a couple of stocks I have my eyes on:

Tapestry ($TPR), the luxury brand company that operates through Coach, Kate Spade, and Stuart Weitzman. P/E ratio of 12.3, pays a 2.57% dividend, and has had decent sales growth over the last five years.

Ralph Lauren Corp. ($RL) sells premium lifestyle products including the well-known Ralph Lauren clothing brand but also sells accessories, home furnishings, and many other soft line products. P/E ratio of 17.3, pays a 2.35% dividend, and has performed great share buybacks of the last 10 years.

Steven Madden Ltd. ($SHOO) designs, markets, and sells fashion-forward footwear through several well-known brands including Steve Madden, Anne Klein, GREATS, and others through wholesale and direct-to-consumer segments. P/E ratio of 11.4, pays a 2.3% dividend, and has shown impressive sales growth over the past decade with the exception of 2020.

Burberry Group PLC ($BURBY) is a holding company that designs, manufactures, and sells apparels and accessories under the luxury Burberry brand. P/E ratio of 21.18, dividend yield of 2% that pays semi-annually, and touts some very stable margins and impressive FCF per share.

I also like Columbia Sportswear ($COLM) but did not dive into them too much as I believe seasonality may dampen the early cycle mover strategy discussed here.

Of these five, I have initiated a small position in Steven Madden Ltd. ($SHOO) and will wait for their earnings report on February 23rd before adding heavy. The reason for this is so that I can get another temperature check on the inventory levels, sales levels, and the margins are trending in the right direction. So far, sales and margins are. Inventory, which is the key, still needs improvement however.

Thank you for reading! If you like pieces like this, follow my Twitter or my CommonStock page where I post updates on the economic data throughout the week. And go check out the 3X discord where I’m actively conversing about ideas like this!

Regards,

Dividend Dollars