This weekly market recap is brought to you by Koyfin, a powerful analytical tool that I am proud to partner with. Their platform is entirely customizable for whatever data you want to look at including stocks, ETFs, mutual funds, currencies, economic data releases (one of my personal favorites used often for these posts), crypto, and even transcripts of company events! Click the link above to get a special offer only for Dividend Dollar readers or go give my product review a read if you’re interested!

Weekly Review

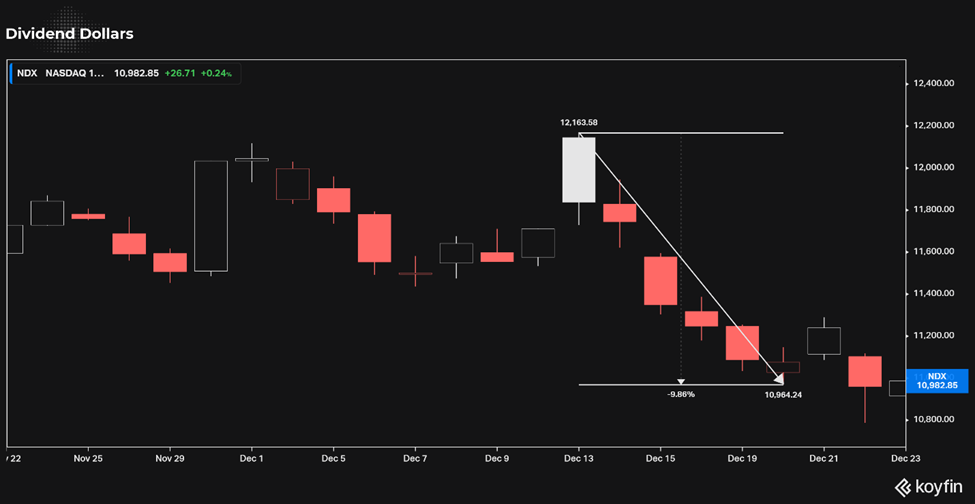

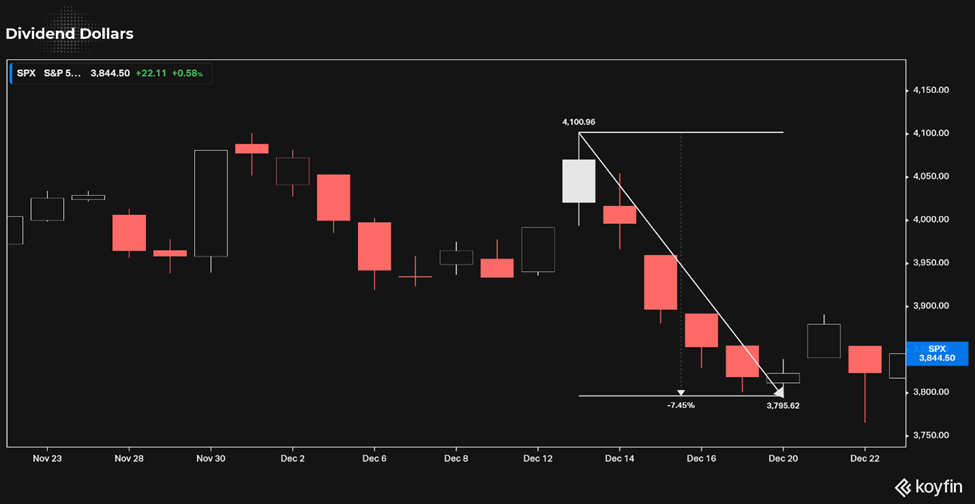

Well, this was a disappointing week, and one that solidifies the absence of a Santa Clause Rally to end the year. The S&P 500, which touched 4,100 last Tuesday, was drawn to the 3,800 level all week which proved to be a key support area.

With tax loss harvesting likely to be beginning and with sentiment falling over all due to 2023 earnings estimates feeling too high, the market was lower this week. Many analysts suggest downward earnings revisions in the coming weeks and months as the economic environment shifts.

The week started on a weaker note as the market digested a weaker-than-expected NAHB Housing Market Index report for December on Monday.

Treasury markets moved on a surprise policy change from the Bank of Japan (BOJ) on Tuesday. The BOJ announced a change to its yield curve control (YCC) policy to allow the 10-yr JGB yield to move +/- 50 basis points from 0.00% versus its prior band of +/- 25 basis points as part of an effort “to improve market functioning.”

This announcement, which came in conjunction with the BOJ’s decision to leave its benchmark rate unchanged at -0.1%, also caused some upheaval for the Nikkei (-2.5%) on Tuesday and the currency market in addition to sovereign bond markets. The yen surged as much as 4.0% against the dollar.

The Market also had to deal with some disappointing housing data before Tuesday’s open, namely an 11.2% month-over-month decline in November building permits (a leading indicator) to a seasonally adjusted annual rate of 1.342 million (consensus 1.480 million).

The S&P 500 dropped below 3,800, scraping 3,795 at Tuesday’s low before buyers showed up for a small rebound effort that ultimately left the main indices with modest gains. At this point, the indices were in a short-term oversold position. At their lows Tuesday morning, the Nasdaq Composite and S&P 500 were down 9.7% and 7.5%, respectively, from their highs last week. That oversold posture triggered some speculative buying interest in a bounce.

Things really took off Wednesday when some well-received earnings reports from Dow component Nike ($NKE) and leading transport company FedEx ($FDX) triggered some decent buying interest.

The market also got some better-than-expected consumer confidence data for December, which was another support factor for the broader market. That report overshadowed a weaker than expected existing home sales report for November that was released at the same time.

Unfortunately, the rebound move soured promptly on Thursday following some disappointing earnings results and commentary from Micron ($MU) and CarMax ($KMX), a sour Leading Economic Indicators report, and some cautious-sounding remarks from influential hedge fund manager David Tepper say he is ‘leaning short’ on the stock market.

He expects the Fed and other central banks to keep tightening and for rates to remain high for a while, making it “difficult for things to go up.” His comments resonated with market participants who recalled the hugely successful “Tepper Bottom” call he made in March 2009.

The resulting retreat was broad in nature with the major indices moving noticeably lower right out of the gate, dealing as well with rate hike concerns after the third estimate for Q3 GDP showed an upward revision to 3.2% from 2.9%. The Nasdaq, S&P 500, and Dow were down 3.7%, 2.9%, and 2.4%, respectively, at Thursday’s lows.

The S&P 500 was stuck below the 3,800 level and Tuesday’s low (3,795) for most of the session before the main indices managed to regain some of their losses in the afternoon trade. There was no specific news catalyst to account for the bounce, possibly just speculative bargain hunting.

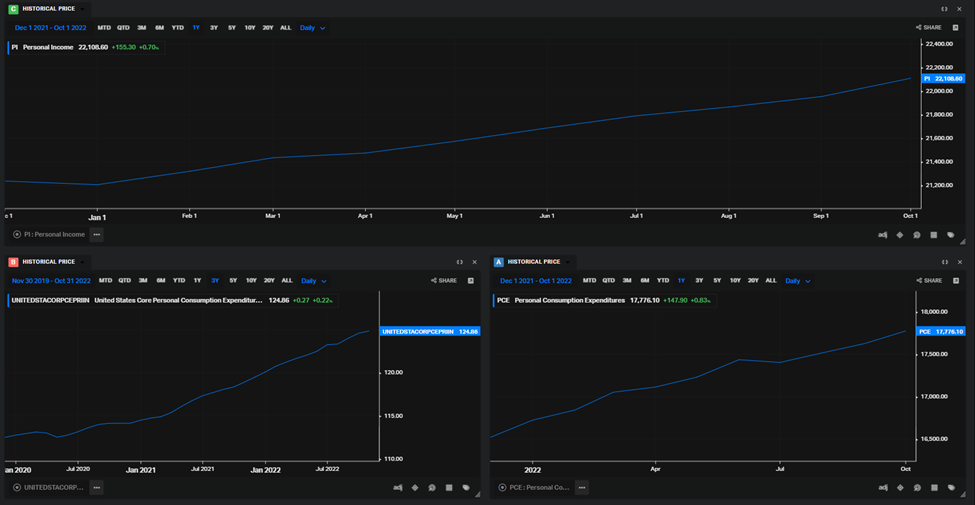

Friday’s session also started on a downbeat note after the November Personal Income and Spending Report showed no growth in real spending and PCE and core-PCE inflation rates that are still too high on a year-over-year basis (5.5% and 4.7%, respectively) for the Fed’s liking.

This report meshed with a Durable Goods Orders Report for November that was weaker than expected and was subsequently followed by economic data that showed new home sales were stronger than expected in November and that easing inflation pressures helped boost consumer sentiment in December.

Once again, the S&P 500 slipped below the 3,800 level, but soon found support as the new home sales and consumer sentiment data bolstered investor sentiment and spurred some bargain hunting interest. The major indices finished modestly higher on Friday, taking a positive first step during the Santa Claus rally period (last five trading days of the year plus the first two trading sessions of the new year).

Separately, the week concluded with the House passing the $1.7 trillion government funding bill after the Senate passed it, leaving it to be signed by the president early next week.

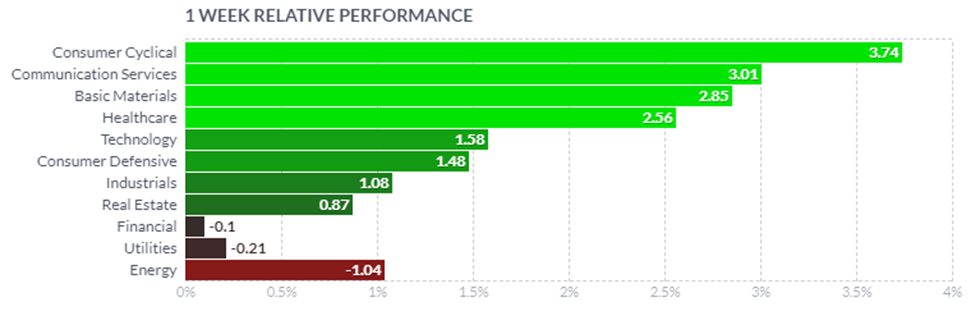

Overall, sector performance was mixed this week with 6 of the 11 sectors in the S&P ending green. Energy, financials, utilities, and a few others finished higher. The weakest links were consumer discretionary and technology which were dragged down by their mega cap components.

Dividend Dollars’ Opinion

That’s it for the recap. Now for my opinion!

Last week I was half-way right in expecting a near term bounce, however I was not expecting it to only last two days (Tuesday and Wednesday). We broke back under the bear market line and stayed there Thursday through Friday.

This here is the key to me. We are under all major moving averages AND the bear market line. There is significantly more resistance than there is support.

Next week, the 3,800 level will be key. We found substantial support at that level as everything under it was just a long wick. There are no major economic releases next week, which make me think we won’t see any crazy catalytic moves in one direction or the other.

We have some claims and housing reports, but that’s about all that’s worth watching, domestically that is. China and Japan have some releases that could bleed over into the US market.

With that, I will just reiterate what I said last week: “With the next earnings season on the way, Fed commentary continuing to spark volatility, and mixed economic data, the next move is anybody’s guess. I think a near-term bounce is likely with more downside to follow after the new year. Then, January will be the month to watch as history shows that it sets the market’s mood for the rest of the year.”

I think the action we saw on Tuesday and Wednesday very well could be the bounce, leaving more downside as my expectation. There are no huge economic releases next week, the Santa Rally so far has been week, therefore I think next week will be red mostly off of tax-loss harvesting.

However, if we open significantly higher in the earlier days of next week, I could see buyers coming in heavy off of the hopes of a strong Santa Rally to push us up through the end of the year. I think this scenario is less likely.

I would love to see more red next week so that I can buy more discounted stocks like I did this week. You can read about my buys in my weekly portfolio update here.

And if you like updates like this, follow my Twitter or my CommonStock page where I post updates on the economic data throughout the week.

Regards,

Dividend Dollars